Select a Section

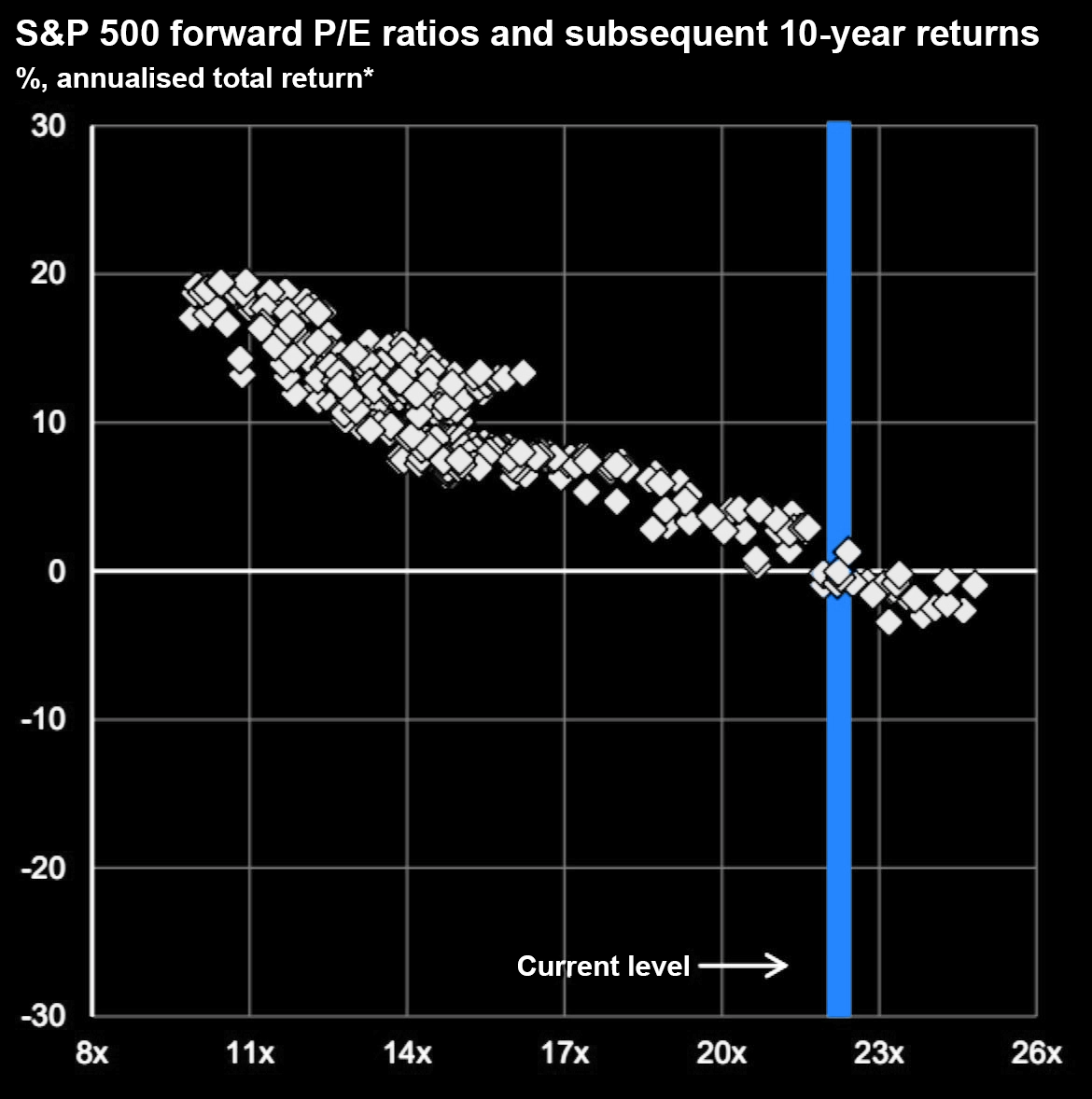

Current State of The Market

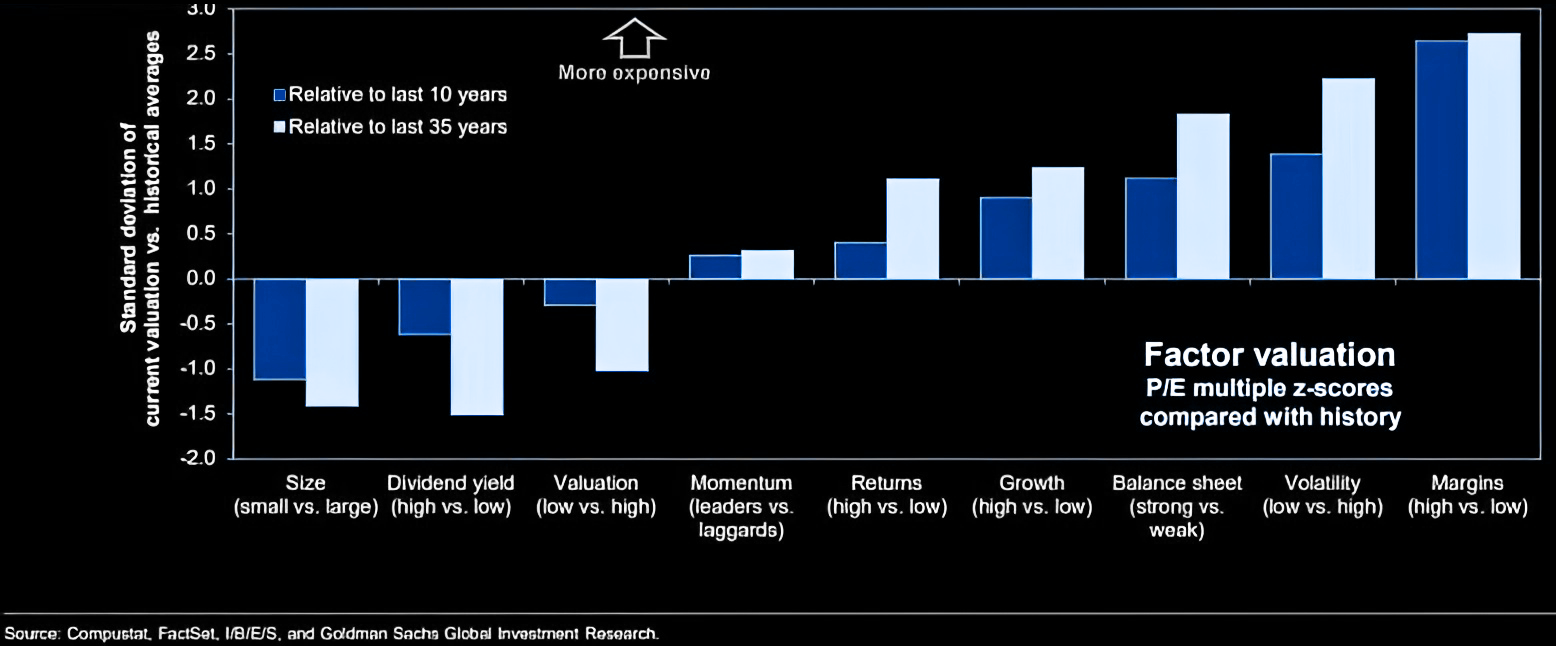

Is the S&P 500 really diversified?

Index weighted 34.6% toward 8 tech companies, with an average 62.8x P/E multiple. Tech concentration is now at peak 2000 levels.

Lessons from History: 2000 Tech Bubble

Burst resulted in an 11 year S&P 500 return of 0% (inclusive of dividends). Capital rotated into previously ignored areas of the market.

Lessons from History: Nifty Fifty Bubble

"Quality" stocks at an average P/E of 42x led to a 2-year, 50% drawdown in the S&P 500. Once again, capital rotated into previously ignored areas of the market. Today’s valuations for US Large-Cap stocks are similar to or exceeding those of the “Nifty Fifty”.

In Summary

Today’s market shares elements of the 2000 Tech Bubble and the 1970s Nifty Fifty Bubble. US Large Cap Growth Stocks may be experiencing a “quality” bubble. We’re told the S&P 500 Index only goes up. In 2007, we were told home prices “only go up”. Conventional wisdom works until it doesn’t.

Current State of The Market: "Barbell"

Companies with High Margins:

Valuations are in the 99th percentile, 2.5 standard deviations above historical averages, relative to companies with lower margins.

Companies with Strong Balance Sheets:

Valuations are in the 95th percentile relative to companies with weaker balance sheets.

Companies with High Growth:

Valuations are in the 88th percentile compared to companies with lower-growth.

Companies with Low Valuations:

Valuations are in the 6th percentile relative to companies with “high valuations”.

Companies with High Dividend Yields:

Valuations are in the 15th percentile relative to companies with low (or no) dividend yield.

Our Perspective

The market is currently a barbell. There’s plenty of value to be found, but it’s probably not in U.S. large-cap or growth stocks. In almost every instance where the S&P 500 has traded at or above current valuation levels, there has historically been a negative total return over the next 10 years.

We believe small caps and “value” stocks have been shunned by the broader investment community and present a much more compelling opportunity.

We don’t know how long the current market dynamic will last, but we would rather be on the receiving end of mean reversion when it does. We don’t know how to time the market, and we’re not interested in trying.

Things We Buy

1. Are entrenched in their respective industries.

2. Generate significant free cash flow and high returns on invested capital.

3. Possess hidden assets whose value is not reflected on the balance sheet, such as long-held real estate.

4. Do not have plausible near-term risk of obsolescence.

5. Are led by management teams with a history of effective capital allocation and demonstrated focus on shareholder value.

6. Have management teams with significant ownership stakes.

7. Are trading at attractive valuations.

Things We Don't Buy

1. Are Unprofitable, unless there’s a prior history of profitability and a clear near-term path back.

2. Are in the current “hot” industry or fad.

3. Require perfect execution in order to justify lofty valuations.

4. Have management teams with a demonstrated history of poor capital allocation decisions, such as investments in low-ROIC or unprofitable ventures, ill-timed share buybacks, or share dilution.

5. Have near-term risk of obsolescence.

Deep

Value

Investing

Deep Value Investing

Deep value investing is an investment strategy that focuses on purchasing securities that are significantly underpriced relative to their intrinsic value. This approach targets companies that are temporarily out of favor or misunderstood but possess strong underlying fundamentals or assets.

Deep Value investing is based on purchasing securities with a large "margin of safety," meaning there’s a cushion between the purchase price and the intrinsic value. This reduces downside risk, offering protection in case market conditions worsen or assumptions about the intrinsic value change. It also offers significant upside potential as securities come to reflect their intrinsic value over time.

Deep value investors seek to benefit from psychological biases in the market, such as overreaction to bad news or herd mentality that drives prices to unsustainably low levels.

Deep value investments can include securities trading at a significant discount to the present value of future cash flow or a significant discount to a company’s tangible assets or liquid assets.

Deep value investing often thrives during periods of market volatility or downturns, when prices are depressed. This creates opportunities to acquire high-quality assets at attractive discounts. It can be seen as a hedge against market exuberance.

Special

Situations

We target unique investment opportunities broadly referred to as “special situations.” These combine deep value characteristics with clear catalysts, offering the potential for outsized returns in overlooked or inefficient corners of the market. Examples of “special situations” could include, but are not limited to:

Special Situations

We target unique investment opportunities broadly referred to as “special situations.” These combine deep value characteristics with clear catalysts, offering the potential for outsized returns in overlooked or inefficient corners of the market. Examples of “special situations” could include, but are not limited to:

Spinoff Transactions

SpinCo can be overlooked or undervalued initially due to forced selling by funds whose mandates do not support it. SpinCo management is often heavily incentivized to increase share price. Lack of awareness and coverage can present substantial mispricing.

Index Deletions

Stocks removed from an index will experience selling pressure as index funds are forced to offload shares. This can result in short–term undervaluation that can be exploited.

Liquidations

Often trade at a discount to liquidation value due to uncertainty of liquidation value and timing. Limited liquidity and, frequently, low market capitalization can limit institutional involvement. These can be great opportunities if we believe we can accurately assess both liquidation value and the expected timeframe.

Restructurings / Post-Bankruptcy Reorganization

Companies often emerge with significantly reduced debt burdens, more streamlined operations, and lower cost structures, amongst other benefits, while still carrying bankruptcy stigma. There may be additional forced selling due to creditors who receive shares in the reorg, but lack interest in holding equity. This can allow us to purchase the new “good” company at prices that reflect the old “bad” company.

Regulatory Changes

Can reshape industries, alter competitive dynamics, or create new markets. Regulatory changes can create “hidden winners” that we may be able to identify before the broader market.

Small and Micro-Cap Advantage

Because of our small relative size compared to other funds and institutions, we have the ability to invest in small capitalization and micro capitalization securities. These can be broadly defined as securities with a market capitalization less than $2 billion and $300 million, respectively. This is advantageous because of:

Limited Institutional Involvement

Institutional investors often avoid small and micro-caps due to regulatory or liquidity constraints. This limits competition to smaller funds and retail investors, which are often less skilled and have fewer resources. In addition, there is often limited or no sell side analyst coverage or media attention, further limiting awareness. Larger opportunity set, less-skilled competition, and structurally greater inefficiency benefits those able to play in this space.

High Ownership by Founders and Insiders

Many small-cap and micro-cap companies are founder-led, with high insider ownership. This alignment of interests can result in decision-making focused on long-term shareholder value.

Attractive Valuations

These securities often trade at valuations far below their larger peers, offering compelling entry points for investors with a long-term view. Market neglect or lack of institutional coverage can result in discounts relative to intrinsic value.

Acquisition Potential

Many small- and micro-cap companies become acquisition targets for larger competitors or private equity firms. Such acquisitions can result in substantial premium payouts for investors.

Case Studies

Saker Aviation Services (SKAS)

Small/Micro-Cap Securities

The Opportunity

In June 2023, SKAS operated as the fixed-base operator (FBO) for the Downtown New York helipad. Customers included tour companies and also high-net worth individuals. SKAS had two key assets: $5M in net cash and a conservative estimated $700k annual free cash flow post-management company removal.

The Thesis

We viewed the risk/reward profile to be exceedingly positive despite SKAS’ potential loss of its helipad concession in upcoming tender. SKAS’ $4.5 million market cap was more than offset by its $5 million net cash, providing ample downside protection.

Potential Scenarios

Downside (-4%):

SKAS loses the helipad concession and liquidates into cash.

Upside (+100%):

SKAS maintains the concession.

Result: ~60% gain in about 6 months, for an IRR of ~150%

CRH plc (CRH)

Building Material Company: "Exchange Arbitrage"

The Opportunity

CRH, a top global building materials provider, was trading at less than two-thirds the valuation of US-listed peers like Martin Marietta and Vulcan Materials, despite being a majority-US operation. CRH’s primary listing on the London Stock Exchange created a valuation gap we recognized as a structural inefficiency—we believed its relisting to the NYSE would cause that gap to close.

The Thesis

The Insight: “Exchange arbitrage” – LSE valuations significantly lag U.S. exchanges. NYSE listing would result in valuation more reflective of peers.

Potential Scenarios

Downside:

Standard market & economic risks.

Upside:

+40% “catch up” in valuation post-relisting

Result: ~65% IRR

Flow Traders (FLOW)

High Frequency Trading Firm

The Opportunity

FLOW is a high frequency trading firm that specializes in exchange-traded products, amongst other asset classes and products.

Dividend Discontinuation

In July 2024, FLOW cut its dividend to increase trading capital, with which they have historically earned 50%-70% returns on equity.

Market Reaction

Dividend cut announcement triggered a sell signal for algorithmic trading programs, causing a 20% decline in share price.

The Thesis

We viewed the cut as a positive development, rather than a negative development, and expected the market to come to the same conclusion once the situation was evaluated and digested by other participants.

Potential Scenarios

Downside (+36%)

Upside (+139%)

Result: Share price increased +39% in 4 months, 150% IRR

Investment Process

Sourcing

Regulatory filings (10-Ks, 13-Fs, 8-Ks, etc.)

Industry experts and our investor network

Quantitative screens and real-time news

Algorithmic keyword tracking, blogs, other social media

Evaluating

Read filings, earnings transcripts, and reports

Speak with experts, test products, and visit locations

Model upside and downside scenarios

Stress Test/ Establish Position

Discuss with other investors or experts in our network

Set clear “thesis-breaking” parameters

Start small, scale as confidence builds

Position Management

Increase / Hold as thesis plays out according to our expectations

Sell: When we believe shares are no long undervalued or when our thesis breaks

Our Fee Structure

Aligned Interests

Limited Partnership, all funds pooled in single entity

Management Fee

1.5% of Assets Under Management (AUM)

Incentive Fee Structure

20% of profit subject to 8% preferred return hurdle

Incentive Fee Structure

20% of profit subject to 8% preferred return hurdle

High Watermark

All incentive fees are subject to high watermark provision

Liquidity & Lock-Up

Year-End Withdrawals, 12-month lockup

Minimum Investment

$100,000 for initial investment. No minimum for additional contributions

Timing

Investments becomes active on the 1st day of the following calendar month

Administrator/Broker

NAV Consulting, Inc / Interactive Brokers LLC

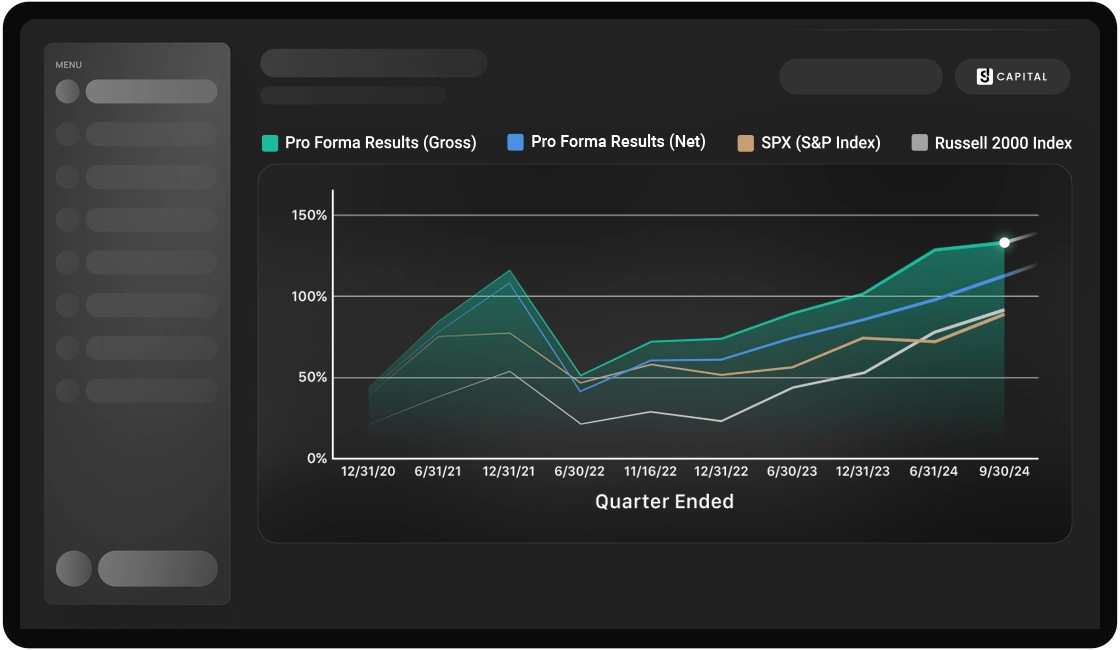

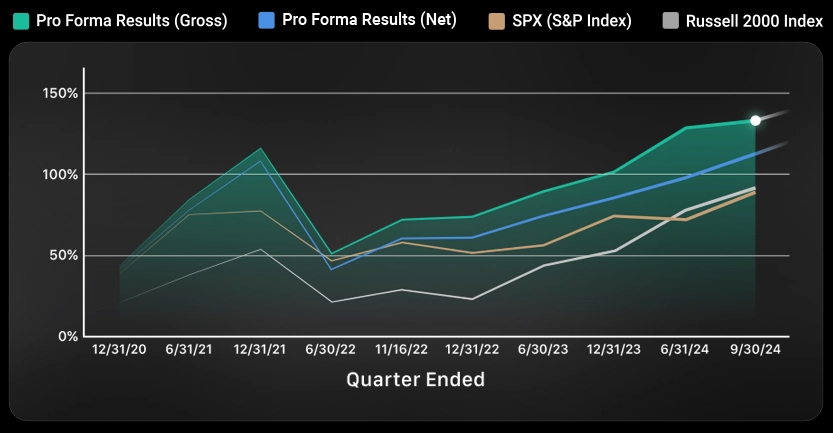

RESULTS THAT SPEAK FOR THEMSELVES

Performance Track Record